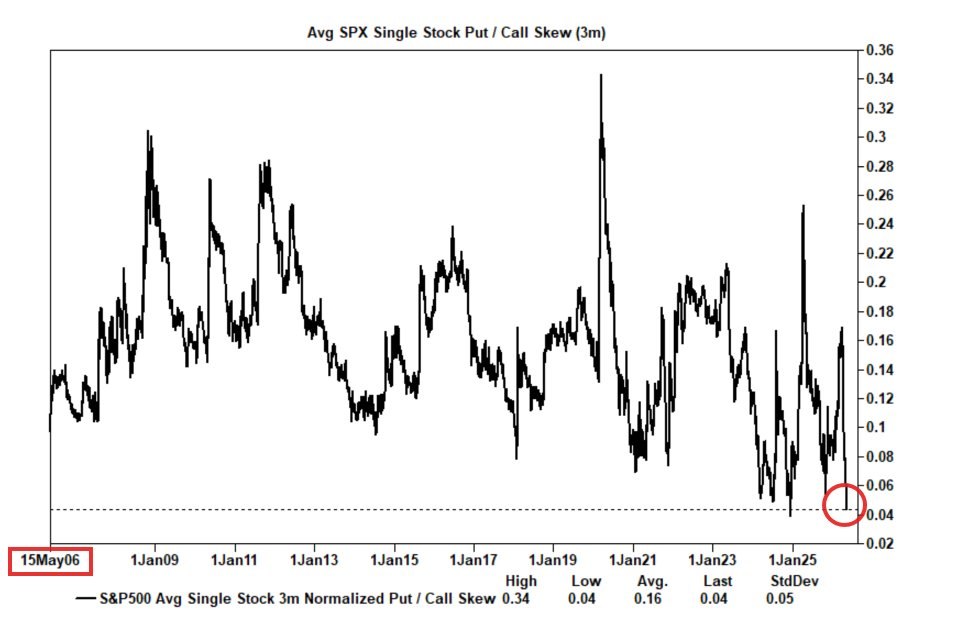

The average 3-month put/call skew for S&P 500 single stocks has fallen to 0.04, marking the second-lowest level since 2006.

The metric measures how much investors are paying for downside protection versus upside speculation. A sharp decline suggests markets are becoming increasingly complacent and overly confident in continued upside.

What makes this more notable is that the collapse in hedging demand comes despite:

Rising Treasury yields

Higher oil prices

Persistent inflation concerns

Escalating geopolitical tensions

Historically, extremely low skew readings have often appeared near major market tops, as investors reduce protection and aggressively chase risk assets.

The latest drop is fueling concerns that equity markets may be underpricing macroeconomic and geopolitical risks while sentiment remains heavily tilted toward an “up only” narrative.

English