In June 2022, the Federal Reserve began quantitative tightening (QT), allowing bonds to mature without reinvestment. This process steadily reduced the Fed’s balance sheet and drained liquidity from the financial system.

Over the following years, approximately $2.4 trillion was withdrawn, bringing the balance sheet down significantly from its peak.

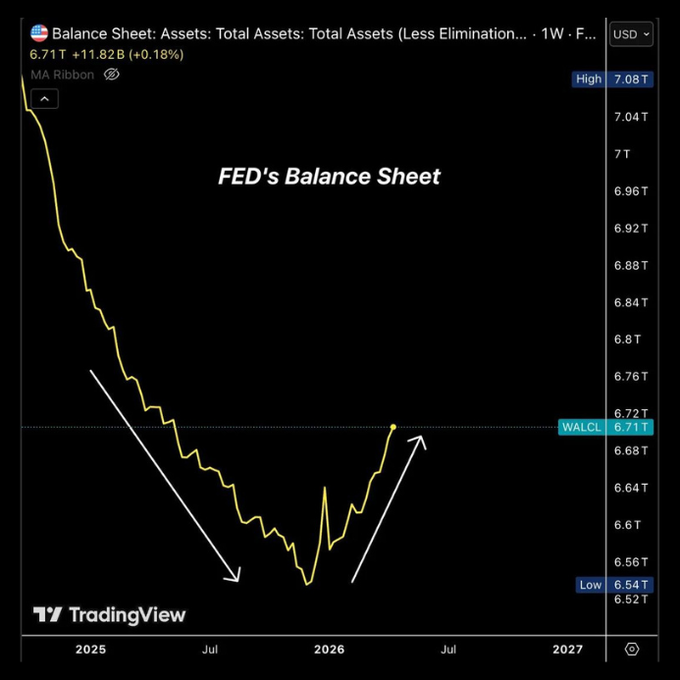

However, in late 2025, that trend came to a halt.

The Fed’s balance sheet bottomed near $6.54 trillion and has since increased to around $6.71 trillion—an expansion of roughly $170 billion from the lows.

Notably, this shift occurred without any formal announcement of quantitative easing (QE) or the launch of a major emergency liquidity program.

Yet, the direction has clearly changed.

This matters because balance sheet expansion injects liquidity into the system. Historically, increased liquidity tends to support risk assets, as excess capital flows into equities, cryptocurrencies, and higher-beta investments.

Since this reversal:

Small-cap stocks have strengthened

Bitcoin has staged a sharp recovery

Overall risk appetite has improved

This does not imply that every market rally is driven by the Fed, but liquidity conditions play a far more significant role than many investors assume.

While most investors focus primarily on interest rates, balance sheet policy often moves markets ahead of rate cuts.

The Federal Reserve may not be easing loudly—but it may already be easing quietly.